N26 has a user experience problem

I love N26’s mission: Mobile banking the world loves. N26 is a Berlin-based “neobank” - a new breed of banks that take a fittingly modern approach to banking:

- mobile-first

- void of physical branches

- actually useful in organizing your finances

- built for the API-powered future of fintech

- the type of easy, responsive support you get with most other SaaS products

Having lived in the UK, I am a former user of Monzo, Starling and Revolut, so I’ve had a chance to become an educated user. There are plenty of other examples neobanks and if you’re interested in learning about then, they’re just a Google search away.

Some background

Germany has a confusing and fragmented card payment landscape. I’m 100% sure I won’t do it justice and again, you can find much more information on this via Google. But I shouldn’t have to care about this. N26 makes me care about it and makes it a problem in my daily life.

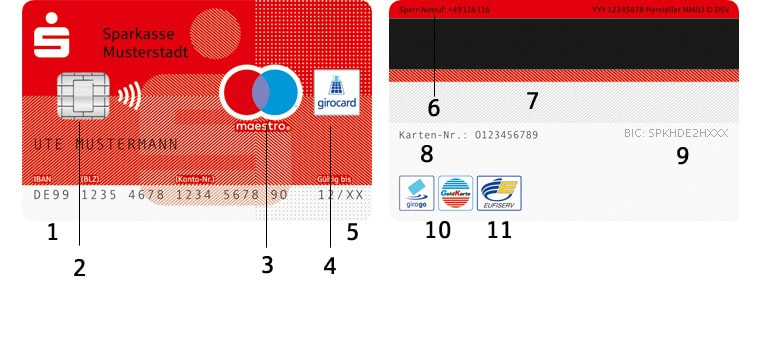

Most residents of Germany will refer to payment cards as either “EC (Electronic Cash) cards” or “credit cards”. This is riddled with confusion and it’s worth unpacking it before we dive into the crux of this UX problem.

Debit Cards

- directly linked to your bank account resulting in transactions being debited from your account immediately.

- Girocard - (formerly EC Card / EC-Karte and by far the most accepted card type in physical shops). EC Card was phased out and replaced with Girocard, Germany’s domestic card payments system. Any major bank in Germany issues debit cards which have Girocard functionality. Those cards will often be co-branded with Maestro, VPay or another payment network.

- Maestro / VPay / Others - These are the other debit card payment systems in Germany. They tend to be accepted less regularly within Germany but regularly outside Germany but within the EU.

- Mastercard / VISA - Debit cards can also carry the Mastercard of VISA symbols. Most Germans will incorrectly assume that such a card is a credit card, but it’s in fact a debit card which allows its transactions to be processed through the Mastercard or VISA networks. This confusion, in large part, is due to the lack of pervasiveness of credit cards in Germany.

Credit Cards

Here I mean true credit cards (Mastercard / VISA / America Express) on which you can carry a balance for a pre-determined amount of time or forever, as long as you make the minimum monthly payment. I’ll skip over these for this post as they’re irrelevant.

Where N26 trips up

Wikipedia tells us that…

User experience (UX or UE) is a person’s emotions and attitudes about using a particular product, system or service. It includes the practical, experiential, affective, meaningful, and valuable aspects of human–computer interaction and product ownership. Additionally, it includes a person’s perceptions of system aspects such as utility, ease of use, and efficiency.

Germany is a wonderful country but when it comes to payment systems, it’s stuck in the dark ages. Yes, even in 2021. Culturally many people prefer cash when making purchases. As such, if a merchant even offers card payments, they likely have an outdated machine which only processes cards with Girocard functionality. This is where the experience as an N26 customer really suffers. N26 doesn’t offer a card with Girocard functionality. In fact, this article on their website makes a point of that. The two standard cards you can request from N26 are:

- debit card running on the Maestro network

- debit card running on the Mastercard network

There are probably good reasons why N26 is missing the Girocard feature. But those reasons aren’t really my problem. My problem is…cortisol.

Cortisol

Because N26 cards are missing Girocard functionality, when I want to pay for things, I never know if my card will be accepted. I carry both N26 cards with me; the Maestro card and the Mastercard. Sometimes merchants have machines that accept one of them. Sometimes they don’t. When they don’t, here’s the choice I’m faced with:

- don’t buy (annoying because I’ve already emotionally committed to buying)

- pay cash (annoying because I really don’t like cash)

- pay with a Girocard-enabled card from another bank (annoying because it means I have to maintain a balance elsewhere just to guarantee my ability to pay and because my payment history is fragmented across multiple accounts)

Annoying. These are all annoying. The brand promise was: Mobile banking the world loves. When my N26 cards get rejected, I hate banking.

I can feel the cortisol (stress hormone) start flowing through my veins every time I attempt to pay with my N26 cards. The worst experience is attempting to pay for parking with cars behind you, but your card getting rejected at the machine. Despite all the effort N26 put into their app experience, their website experience, their smartphone-powered identification/onboarding experience and their branded paid subscriptions, they have failed to address this basic, primitive use-case: I want to buy something with my card.

Make me a tribe member!

Cortisol kills the experience for me. It undermines all the silky-smooth experience N26 agonized to deliver to me. I curse N26 under by breath in those moments instead of belonging to the N26 tribe. Then I recover. It’s a emotional rollercoaster. Monzo, for its part, has done an amazing job of building a community of enthusiastic evangelists.

The truth

The point here is that despite the noble mission, the great app, the solid service and insights into my spending, the truth of the German payments landscape is not such that you can get away without a Girocard. N26 has allowed its UX to be undermined because it has not accommodated this truth. The reasons for that are irrelevant. All that remains is the experience.

I know I’m not as much of an N26-tribe member as I could be. Certainly not as much as I was a Monzo-tribe member. I suspect many feel this way. I don’t recommend N26 to anyone, although I still prefer them to the big, inept banks. When you recommend a product, you risk your social capital. I don’t want to be the one my friends associate with the stress of not being able to pay for parking and getting honked at.

This is an interesting case study on where product decisions and technical limitations connect directly with brand promise. Or rather, when they undermine it. N26 can fix this problem and I’ll be a happier user when they do.